- ebook

- Wednesday, October 28th, 2015

- open networks

-

In my last posting, regarding home bias and the difficulty of seeing past familiar territory to other possibilities,the research puzzle | Believe it or not, the second season of Fargo is based in my hometown, which is what spawned that posting. I promised to provide some thoughts on how to get more information from the outside.

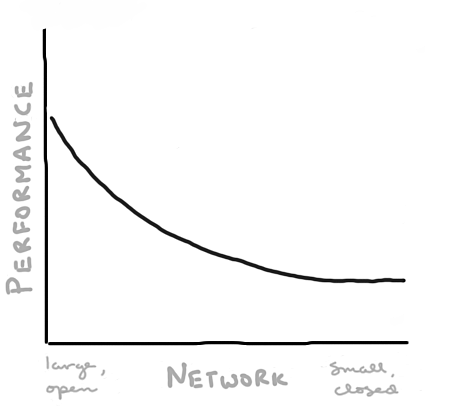

A piece by Michael Simmons, “The No. 1 Predictor of Career Success According to Network Science,”Observer | Simmons is the co-founder of Empact; its goal is to “alleviate mental & financial poverty.” included a graphic that looks roughly like this:

Simmons wrote: “Most people spend their careers in closed networks; networks of people who already know each other. People often stay in the same industry, the same religion, and the same political party. In a closed network, it's easier to get things done because you've built up trust, and you know all the shorthand terms and unspoken rules. It's comfortable because the group converges on the same ways of seeing the world that confirm your own.” But . . .

That straightjackets us. The real breakthroughs come when you have an open network on which to draw. In the article, Simmons used Steve Jobs as an example of someone who took vastly different experiences and connections in his life to foster unique, game-changing (OK, world-changing) ideas.

“Creativity is just connecting things,” Jobs said.

The subject of networks has been touched on in past essays here, including in response to ideas from Paul Pedrazzithe research puzzle | The piece was called “the social urge,” because new social networking ideas were cropping up everywhere at the time. at the Defrag conference in 2008, Brian Uzzithe research puzzle | This was part of a very long series of postings from that conference. at the CFA annual conference in 2012 (funny how their names both end in “zzi”), and Gjergji Cici, et al.,the research puzzle | In it, I encouraged those analyzing such organizations to look at the hidden networks in addition to the ones on organizational charts. regarding the propagation of positions and ideas within mutual fund organizations.

The typical investment person, when seeing the chart above, would immediately glom onto the “performance” label on the Y-axis. Could it be a reasonable graph in regards to investment performance as well as career success? I think, “Yes.”

I would qualify that answer in this way, however: the chart as laid out combines “large” and “open” on one end of the scale — and “small” and “closed” on the other. I think that most people in the investment world have quite large networks, but very closed ones in terms of the range of ideas that are exchanged. The discourse is narrow, focused on the business of making money.

Therefore, if you crossed out “large” and “small,” and just had “open” and “closed,” I think that the graph fits. Investment professionals and organizations suffer when their networks are too closed.

Some examples:

~ Most investment people are isolated within their own organizations. By not interacting with other departments, they lose sight of the real purpose of the organization and foster a balkanization that works against its success.

~ There is undue specialization within the business and an unrelenting pursuit of relative performance, creating a powerful but tight frame of reference for individual actors that works against the consideration of those outside the game and their ideas.

~ The worlds of asset management, investment advice, and institutional investing intersect with each other, but developments within each are often treated as separate (if they are seen at all), when they are actually parts of a whole.

Those examples highlight tendencies within the confines of the investment world itself. More to the point of truly open networks, there are very few nodes of contact with other disciplines and ways of thinking. That translates into a narrow field of vision.

It seems to me that most investment professionals judge the power of a network in terms of the power of the contacts within it, and there is some truth to that. But that power is easily shared by others. Some might get special access or early insight, but only a few can leverage it consistently; there are too many others chasing the same goal in the same way.

Individuals should consider whether they can have any lasting success at that me-too game, or whether building networks that are truly different than those of others might provide a side door to the alpha store. Unfortunately, building those kinds of networks doesn’t come easily to many people, and certainly not to most investment professionals.

In contrast, the designers of investment organizations can create an environment where it’s more likely to happen. (That would be more obvious if “the designers of investment organizations” wasn’t such a foreign concept to those in charge.) This is an information business, but buying the same terminals with the same data as everyone else and being on the same calls and reading the same research doesn’t provide an edge, it makes you part of the pack.

Open networks don’t guarantee anything, but they at least offer the opportunity for discovery and, with it, a potential pass out of mediocrity.